The UK Patent Box is a generous scheme that can yield significant savings for UK companies. By electing for Patent Box tax treatment, UK companies can benefit from a reduced rate of Corporation Tax of 10% on a proportion of profits derived from qualifying intellectual property (IP) rights.

The basic concept is straightforward but, as ever, there is some complexity in the detail. The purpose of this briefing note is to strip out some of that complexity and give companies a clearer idea of what they can do to ensure eligibility for, and maximum benefit from, Patent Box.

Understanding Patent Box

Who is eligible?

To be eligible for Patent Box a company must:

- Be liable to pay UK Corporation Tax.

- Own a qualifying IP right or hold an exclusive licence for a qualifying IP right (the exclusivity may relate to a particular national territory or different fields of application).

- Satisfy the ‘development condition’ by showing that the company has significantly contributed to the creation of the invention or has developed it or developed its application, even if the qualifying IP was acquired. If a company is a member of a group and only a fellow group company satisfies the development condition, the company can instead show that they have performed significant management activity in relation to the IP rights.

What IP rights qualify?

Profits derived from the following patents can benefit from the Patent Box regime:

- Patents granted by the UK Intellectual Property Office.

- Patents granted by the European Patent Office – regardless of where they are validated.

- Patents granted in EEA states with similar patentability and examination criteria to the UK. As of April 2021, these are Austria, Bulgaria, Czech Republic, Denmark, Estonia, Finland, Germany, Hungary, Poland, Portugal, Romania, Slovakia and Sweden.

The regime also applies to other, less common IP rights such as Supplementary Protection Certificates and European Community Plant Variety rights, but it does not extend to Utility Models, Registered Designs or Trade marks.

A patent must be granted to qualify. However, once the patent is granted, the income derived from the patent while it was pending can be included in Patent Box for up to six years prior to grant. Once the patent has granted, the benefit will be calculated based on the later of the IP filing date and the accounting period in which the company elected into the Patent Box regime.

What are the benefits?

Patent Box is designed to incentivise and reward the commercialisation of IP through a reduction in Corporation Tax. Eligible companies can benefit from a reduced rate of 10% Corporation Tax on a proportion of their profits, referred to as Patent Box Profits.

What income can be included in the calculation of Patent Box Profits?

Patent Box Profits are calculated based on ‘relevant IP income’ (RIPI). In the case of patents, RIPI is income derived from any of the following:

- The sale of the patent itself

- The licensing of the patent (royalty income)

- The sale of the patented invention

- The sale of goods which incorporate the patented invention

- The sale of goods that are designed to be incorporated into the patented invention (such as cartridges, power packs or replacement parts)

- Infringement income and damages from legal cases and settlements

- Use of the patented invention to produce non-patented products (for example using a patented machine to make non-patented items)

- Services which incorporate the patented invention (such as a patented tool or instrument used in vehicle servicing)

Note that in these latter two cases there is a different method of calculating profits based on a notional royalty akin to the royalty that would be paid to an independent owner of the IP for its exclusive use.

Notably, once there is a qualifying patent in place, all worldwide income can be within the Patent Box calculation – the sale or licence need not be in the jurisdiction of the qualifying IP right.

How are Patent Box Profits calculated?

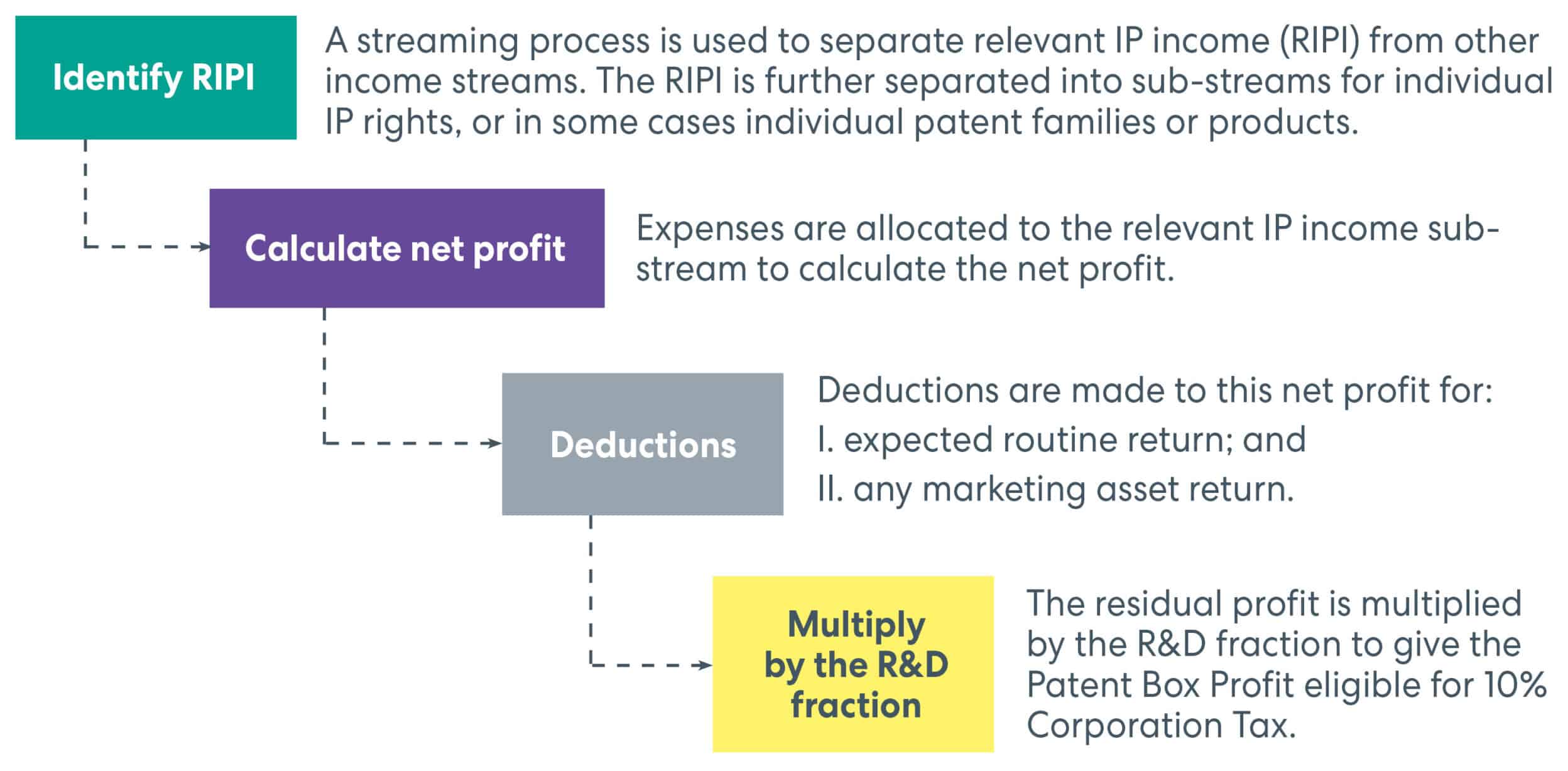

Patent Box Profits are calculated in 4 steps: What is the R&D fraction?

What is the R&D fraction?

The R&D fraction, also referred to as the nexus fraction, is the proportion of the net profits that can benefit from the reduced tax rate. It is calculated for each sub-stream based on the relevant R&D expenditure incurred by the company holding the qualifying IP. Its purpose is to ensure that the companies benefitting from Patent Box are investing in substantial activities related to IP development, either directly or by subcontracting to a third party.

To calculate the R&D fraction, companies are required to keep a detailed record of all relevant R&D costs associated with their qualifying IP. The maximum fraction of 1 is achieved if 70% or more of the relevant costs are for in-house R&D or R&D that is sub-contracted to a third party. The fraction is reduced below 1 if more than 30% of the relevant costs are for acquisition, exclusive licencing or R&D that is sub-contracted to a connected party.

Maximising your potential benefit

How can I take advantage of Patent Box?

There are many ways in which a patent filing strategy can be adapted to maximise your potential benefit. The following considerations provide a good starting point:

- What are the patents behind your income streams? Think widely here about all of your income streams and look at ways to connect them back to patents. This could involve keeping a detailed record of how the company’s patents relate to products that are being developed and used.

- Are the patents that you have identified qualifying or non-qualifying patents? If you have income that derives from non-qualifying patents, then it may be possible to improve this position.

- Are the patents granted or pending? For pending patents, election into Patent Box will enable you to include some pre-grant profits once the patent has granted. It may be possible to accelerate grant in order to qualify for Patent Box relief sooner.

- Do you own the patents or have an exclusive licence? Consider renegotiating the terms of your licensing agreements to qualify.

- Have you sold or licensed any qualifying patents?

- Do you have qualifying patents which could be licensed to create new revenue streams?

- Can you satisfy the development condition?

- Are you inventing solutions to internal manufacturing and production problems? It may be that these are patentable and can bring additional Patent Box benefits.

- Don’t currently have any patents or patent applications? Look closely at your products and processes to see whether patenting may be possible. Remember that one qualifying patent may suffice to secure Patent Box tax treatment for all of the worldwide income from an invention.

How HLK can help

HLK was closely involved in HM Government’s initial Patent Box consultation process and is one of the very few IP firms to have helped shape the legislation. As a result, we have a deep understanding of the new regime and of how UK companies can benefit from it.

HLK can review your IP portfolio and your patenting strategy to ensure that relevant patents or patent applications within your existing portfolio are identified and that plans are in place to patent key product technologies in future in order to benefit fully from the Patent Box. We can also advise on the range of inventions which can be patented, which may be broader than you think.

Thanks to the Patent Box regime, patents can be used not only to prevent third parties from exploiting an invention, but also to reduce the tax burden. Thus, a patent filing strategy should take account of the opportunity for a reduced tax bill as well as the wider strategic goals of the business in protecting and exploiting its innovations.

Sources of Further Information and Advice

This is for general information only and does not constitute legal advice. Should you require advice on this or any other topic then please contact your usual HLK advisor or our Patent Box team:

Andrew Dowling

Partner

adowling@hlk-ip.com

Phil Davies

Partner

pdavies@hlk-ip.com

A PDF of this information can be accessed here.